Before any commercial flight takes off, all passengers are reminded of a crucial safety rule: if the cabin loses pressure, make sure to put on your own oxygen mask before assisting others. It's a part of the air travel experience that many passengers are so used to that they now just throw on their headphones and crank up the volume to drown it out.

It might seem selfish at first, but securing your own mask before helping others is important and it’s not because the airlines say so. Instead, it’s based on a simple logic — it's a lot harder to be helpful to anyone if you need help yourself!

This logic can be applied to finances, too. If you can’t breathe financially, you won’t be able to help others.

So, before you make a loan to a friend or family member, keep in mind these three things to make sure you can keep your head above water first before helping out others 👇

Build up your cash reserves

Well, you might be asking yourself, “How much money can I lend to a family member?” Well, the answer all depends on how much cash you have reserved for a rainy day.

Most financial advisors recommend having at least 3 to 6 months of living expenses saved up in cash as a safety net. Obviously, this is easier said than done, but taking steps toward that goal is key. If you aren’t yet able to make a family loan, start building your own savings.

At the start of each month, set aside 5-10% of your earnings as savings. To help build your stockpile, explore ways you can raise cash quickly, but make sure to steer clear of any pitfalls you may see.

Once you have some money saved up, don’t just keep your dough under the mattress — find a place to store it that suits your needs. If you find yourself out of a job or unexpectedly in the hospital, this extra cash will prevent you from going into debt or selling assets.

To keep it simple, ask yourself this single question: if your income disappeared tomorrow, how long could you last? 🤔

This question is important to ask yourself, especially when considering the loan amount you are willing to give your friend or family. While you could eat rice and beans for every meal if things went south, let’s be realistic - essentials like rent, utilities, and childcare costs are going to be hard to cut.

To help figure out how you could spend less to build your cash reserves, try the following exercise:

- Add up your essential monthly expenses. Rent, utilities, groceries, and insurance are included here.

- Take notice of monthly costs that are not necessary. Personal finance tools like TrueBill make this easy as pie to visualize. Ask yourself, when in a pinch, which costs would I prioritize? Add those to your expenses total.

- Review the rest of your spending in the last few months. Take note of irregular expenses, like vehicle maintenance, and be honest with yourself about what types of other purchases you could live without. Add the most essential expenses to your total.

Once you have a handle on your minimum monthly budget, compare that total to your cash on hand. If your current cash balance wouldn’t last you three months, focus on building your reserves before lending to others.

Get smart with your debts

Vicious debt cycles can trap people in financial holes for a long time, and it’s far easier to avoid them in the first place than to dig yourself out of one.

If you’re currently buried under a mountain of debt, whether it be from credit cards, student loans, or medical care, you can’t afford to lose more money. However, all debts aren’t created equally.

Mortgages, for example, are one of the most common types of debt, and tend to have low interest rates and favorable loan terms. Credit card debt, on the other hand, can spiral out of control with just a few missed payments, and charge interest rates as high as 20%.

If you’re suffocating under a debt burden, here’s a snowy strategy to introduce you to:

Behold the debt avalanche.

The debt avalanche is a strategy to help you relieve yourself of your debt burden. It works like this:

- Put your debts in order by interest rate from highest to lowest.

- Make the minimum payment on all of your debts, and use any leftover cash to pay down your highest-interest debt.

- Once the highest-interest debt is paid off, take the extra budget (i.e. from having one less minimum payment) and add it to the monthly payment going towards your second-highest debt.

- Repeat until all debts are paid, or until your debt is at a manageable level.

By paying off high-interest debt first, you’ll ensure that your payments are actually paying down what you owe, rather than just covering the monthly interest. Think of it like swimming toward an island instead of treading water. Trying to tread water while helping out family and friends is probably not a good idea, you honestly may end up having to yourself if you’re not careful.

Cash is like oxygen: it’s a precious resource that keeps your financial life alive. A few minutes underwater can be survived, but past that, well…💀

Get inside your own head

A 2021 survey from Capital One found that nearly three-quarters of Americans point to money as their number one stress in life. Pandemics, work, and geopolitics all take a back seat to the almighty dollar.

We all react to stress differently. Some lie awake all night, while others may have an anxiety producing voice in the back of their head.

It’s good to know how you should respond.

If you’re able to handle emotionally stressful topics like money, then is a great way to support those around you. Whether you’re the borrower or lender in any scenario, mixing money with your familial relationship can make things more stressful. If stress regarding money consumes all of your waking hours, then it may warrant a second thought to take it to the next level.

If you’re a chronic stressor and are asking yourself “is lending money to family or friends ever a good decision?” then maybe you should have an honest conversation with yourself. Was your family financially insecure growing up? Do you have any irrational fears about losing everything? In these cases, honest conversations with confidants or even therapy can help you achieve a healthier money mindset.

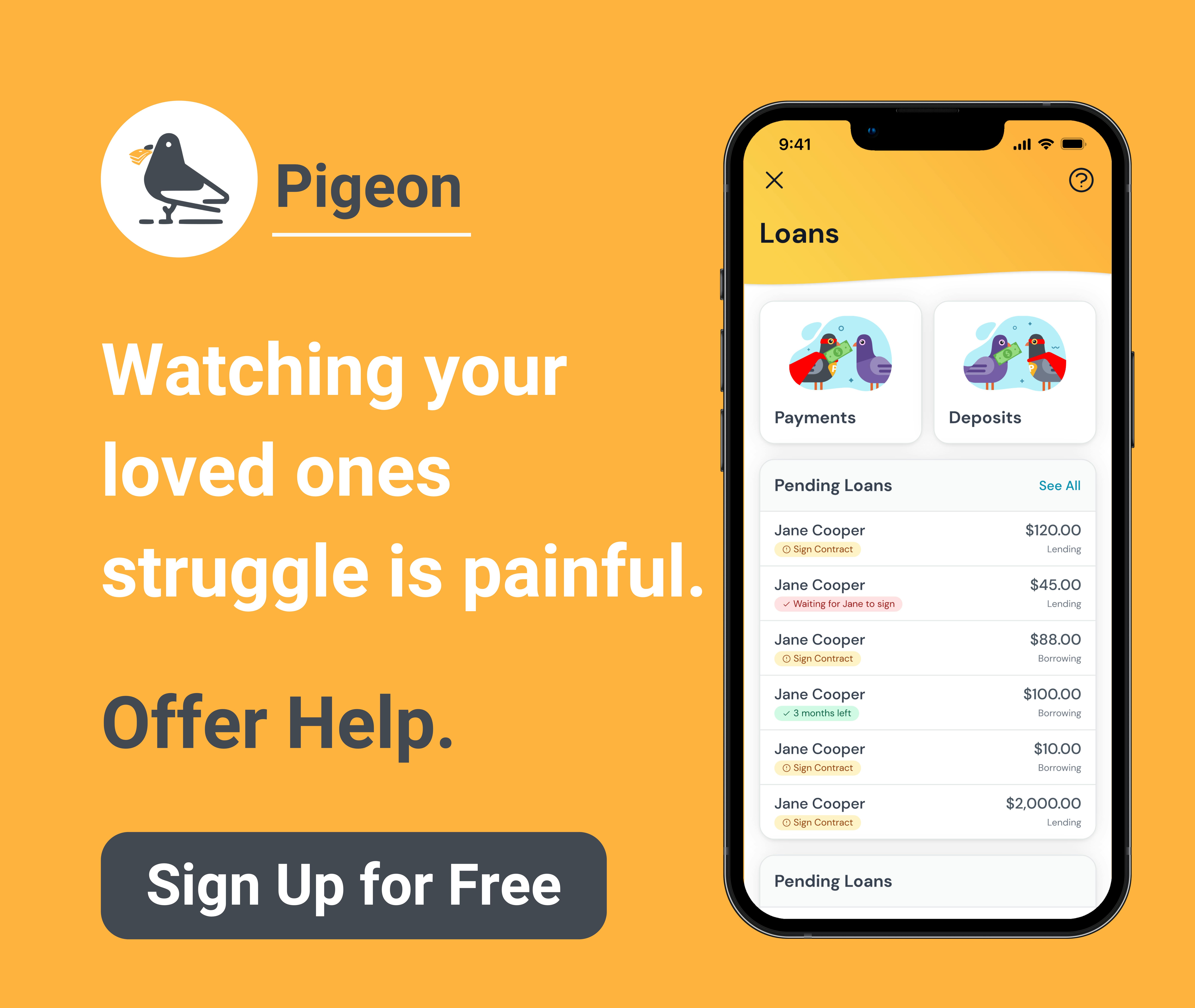

Make sure you develop a healthy attitude towards your wallet before lending to others. Tools from Pigeon can also help bring peace of mind to either side of the conversation. Whether you are issuing out a business loan or offering a personal loan to your family, having a written agreement and clear expectations can do a world of good for you when dealing with family loans.

Help yourself before helping others

Lending money to friends and family in times of need is a fulfilling way to support those you care about. You shouldn’t have to ask yourself, “Should I lend my family members money?” and feel helpless or lost because of wanting to do a good deed.

We’ve all had unexpected expenses pop up, and know how stressful those times can be.

If a loved one is truly in need, then taking the time to help can sometimes literally mean saving their life.

Keep this checklist in mind next time a friend asks for you for a loan:

- Do I have 3-6 months of expenses saved in cash?

- Given my income, is my current debt level manageable?

- Am I mentally prepared to loan my family member money?

Once you’ve checked off all these boxes, you might want to use Pigeon to create a loan agreement all parties agree on, or even just to give yourself a stress-free way to keep track of everything from payments to reminders all in one place.

You won’t be much help to others if your own finances are out of whack, so get your own financial house in order first, and once that’s done, you’ll be well on your way to helping friends & family do the same. 👏

Want to read more related content? Check out some more of our awesome educational pieces below: